Why Keynesian Central Bankers Never Say They’re Sorry

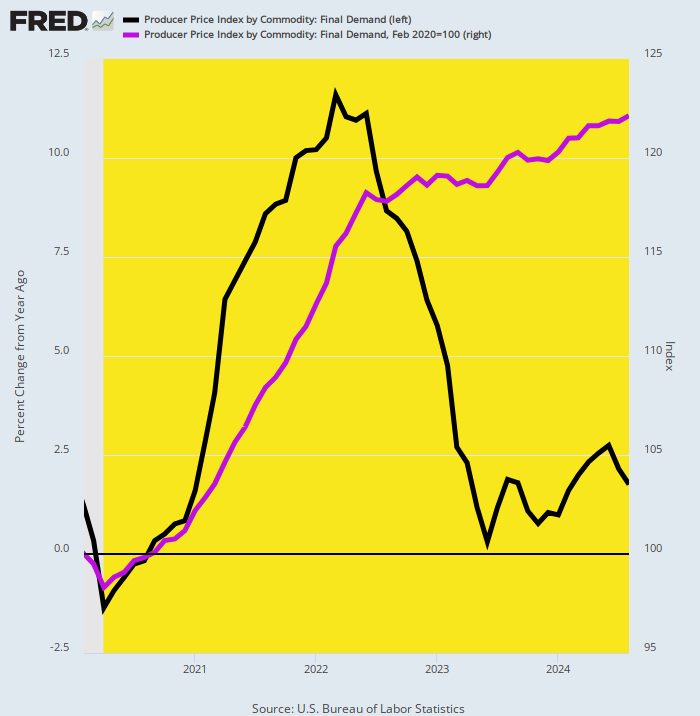

Our Keynesian monetary central planners never say I’m sorry—they just make excuses until they can cherry-pick the data to show that their destructive policies are working. Today’s producer price report for August, which showed Y/Y change in the PPI final demand index (black line) of just 1.76%, is surely a case in point.

Wall Street is chirping ever louder for rate “cuts”, so this tame reading is being flogged as still another reason for the Fed to hit the rate cut button at next week’s meeting. Then again, why should the purported guardian of the nation’s money view a cumulative 22% rise in the same PPI index (purple line) just since February 2020 as a sign of success and signal to restart the printing presses?

After all, if you carry the inflation trend embedded in the purple line, which computes to 4.5% per annum, forward for just one decade today’s dollar is worth just 63 cents at the end point. Yet where is the evidence that 63 cent dollars a mere decade hence would be good for productivity, investment, economic growth and real living standards?

Or, on the other hand, why would 63 cent dollars be even remotely equitable in their impact among different classes and segments of economic actors? For instance, as among—

savers versus borrowers.

workers in globally competitive industries vs. bureaucrats on the payroll of monopolistic government agencies.

fixed income retirees vs. corporate executive bonus babies.

entrepreneurs and self-employed in cyclical industries vs. payrollers in the stable utilities, health and education sectors, among countless others.

Index Of Final Demand PPI and Y/Y Rate Of Change, February 2020 to August 2024

Actually, a mere glance at the above chart conveys the wicked shell game the monetary central planners and their shills on Wall Street play with the inflation data, and, indeed, all the other alleged “in-coming data”. Almost without exception the economic data is viewed in terms of the rate of change on a running monthly, three-month, six-month or Y/Y basis. That is, all the focus is on the black line or delta, even as the purple line or level is virtually ignored.

In other words, in August 2024 you don’t have to say your sorry about the 11.6% Y/Y shellacking that a buyer took in March 2022 per the black line above or the fact that the February 2020 dollar will buy just 81 cents at wholesale today. As far as the Keynesian apparatchiks who run the central bank are concerned, those consumer beatings are in the rear-view mirror—ancient history that is over and done.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.