Why “Contagion” Ain’t What It’s Cracked-Up To Be

The Fed is so far behind the inflation curve that it can’t even see the tail lights. So it deserves no praise whatsoever for sticking with its belated tightening game plan by raising rates another 25 basis points.

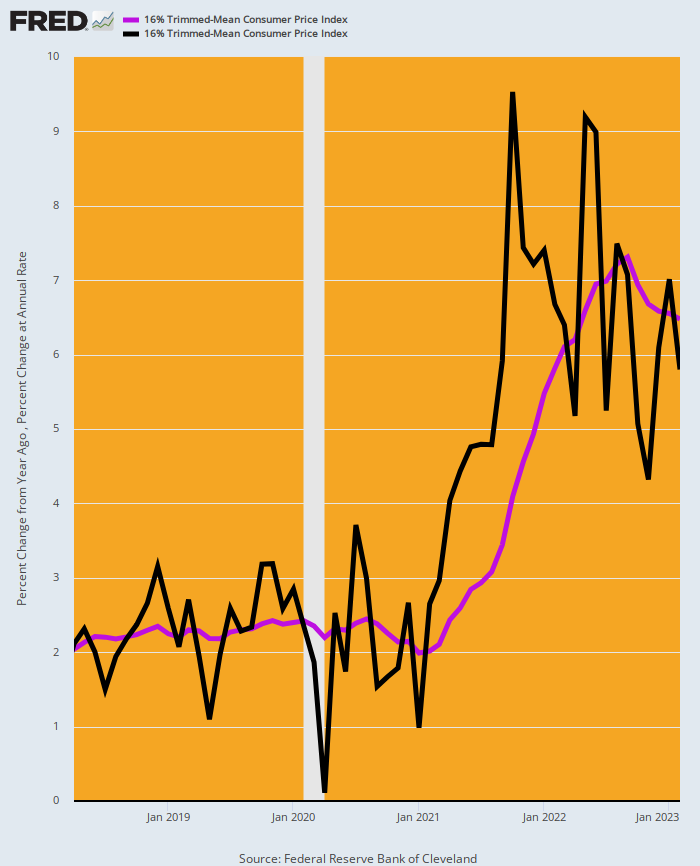

In fact, the Fed funds rate will likely settle at about 4.9%, which is still way the hell under the running inflation rate. Again, here is our trusty 16% trimmed mean CPI. The graph shows that the inflation rate has been continuously above the Fed’s 2.00% target on a Y/Y basis since April 2018, and now stands at 6.5% Y/Y or more than triple the target.

And, no, inflation isn’t suddenly evaporating like the morning dew. It was up by 5.8% on an annualized basis in February, has averaged 6.3% for the past three months and 6.1% since the peak in June 2022.

So the inflation rate is running at 6.0%+ no matter how you slice it, and that is an economic no-no. It implies that the value of a dollar of savings would decline by 46% over a ten-year period.

That’s right. At the end of the day true, sustainable capitalist prosperity depends upon robust private savings. But for all practical purposes, the current inflation rate is wiping-out half of savings every decade.

CPI Inflation Rate: Y/Y And Monthly Annualized, 2018 to 2023

Likewise, the implication of a 6%+ inflation run rate is that the real Federal funds rate will still be more than -1.0% after today’s action. Yet that’s not the half of it.

The real problem is that the Fed funds rate has been continuously negative in real terms since October 2009, save for two short intervals when its was allowed to peek above the zero bound for a fleeting few months. That amounts to an unprecedented 160 month interval during which ultra-cheap money was being flooded into the financial system at the command of the Eccles Building.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.