We Don’t Need Three More Stinkin’ Rate Cuts

Jerome Powell is not completely the blithering idiot he seems. Actually, playing the role of chairman of our monetary central planning agency would have done that to anyone— even Einstein.

After all, we are talking about monetary Mission Impossible here. There is an infinitely complex and opaque $26 trillion economy in America, which is deeply and intricately interwoven with a $105 trillion global GDP. As such, the US economy operates far, far beyond the reach of any would be state administrator, planner or economic czar.

In part that’s because the “incoming economic data” on the Fed’s dashboards is unreliable, incomplete, noise-ridden and frequently undecipherable. Likewise, its tools of policy implementation and control are crude, wobbly and generally unfit for purpose.

So the Fed is pleased to pretend it is precisely and scientifically pursuing macroeconomic “goals” with respect to inflation, full employment and general maximization of prosperity, thereby bestowing the greater good on main street America. But that’s a ruse. In fact, what it actually does is to periodically bend over when Wall Street hands it the proverbial bar of soap.

Yesterday occasioned the latest ignominious episode of this monetary whoredom when Powell pivoted on a dime with respect to rate cuts, thereby flushing down the memory hole his own position of just two weeks earlier. As Zero Hedge noted,

One day after the Fed’s bizarre, unexpected pivot, many are struggling to wrap their heads around what happened: what exactly changed in less than two weeks for Powell to go from telling the market it was “premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease” to suddenly warning that rate cuts are something “that begins to come into view, and is clearly a topic of discussion out in the world and also a discussion for us at our meeting today.”

Even Powell’s own mouthpiece, WSJ reporter Nick “Nikileaks” Timiraos, was confused remarking sarcastically after the FOMC “what a difference two weeks can make.“

So to reprise Wednesday’s post: Inflation hasn’t been vanquished, real interest rates are still deeply subnormal and $8 trillion of fiat money production since 2008 is more than enough for decades to come. So why is Powell even talking about rate cuts?

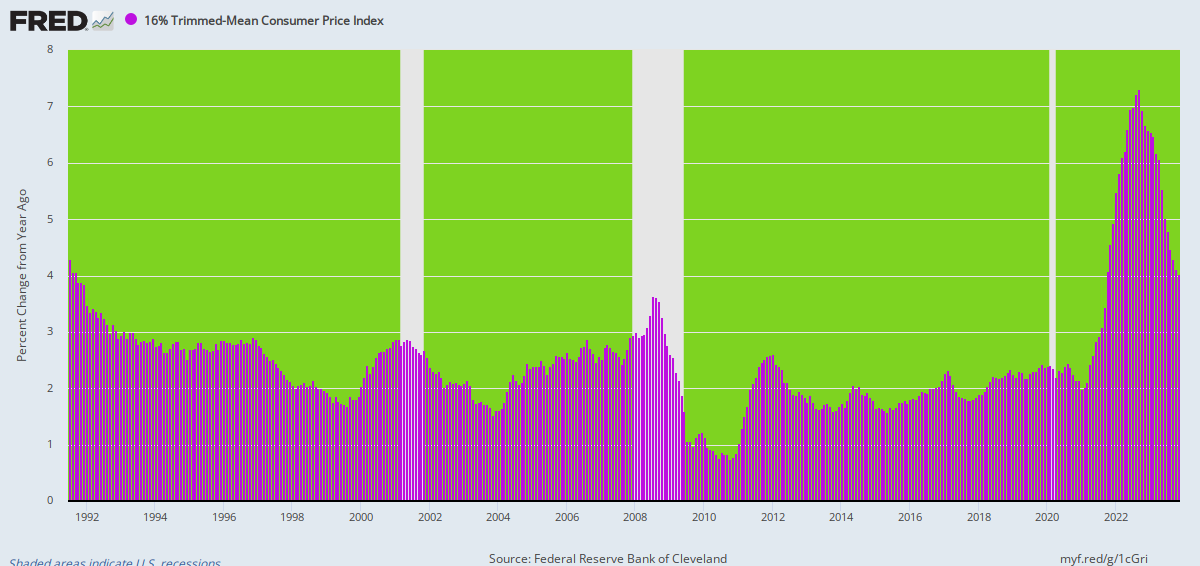

Y/Y Change In 16% Trimmed Mean CPI, 1991 to 2023—At 4.0% Still Highest Trend Rate In 32 Years

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.