The Trumpian Myth Of Global Grand Theft, Part 2

Once the global central banking system had essentially been transformed into a beggar-thy-neighbor FX management and manipulation racket, it didn’t take long for many foreign central banks to basically adopt a “see and raise” posture. That is, not only did their pegging operations aim to match the Fed’s prodigious money-printing and thereby keep their exchange rates from appreciating against the dollar, they actually attempted to push their FX rates lower.

In a sense, the post-1971 Fed had declared open season on bad central bank money. Its reckless expansion of dollar liabilities was bound to be followed by aggressive money-printing in the rest of the world because the short-run consequences of not doing so were too unpleasant.

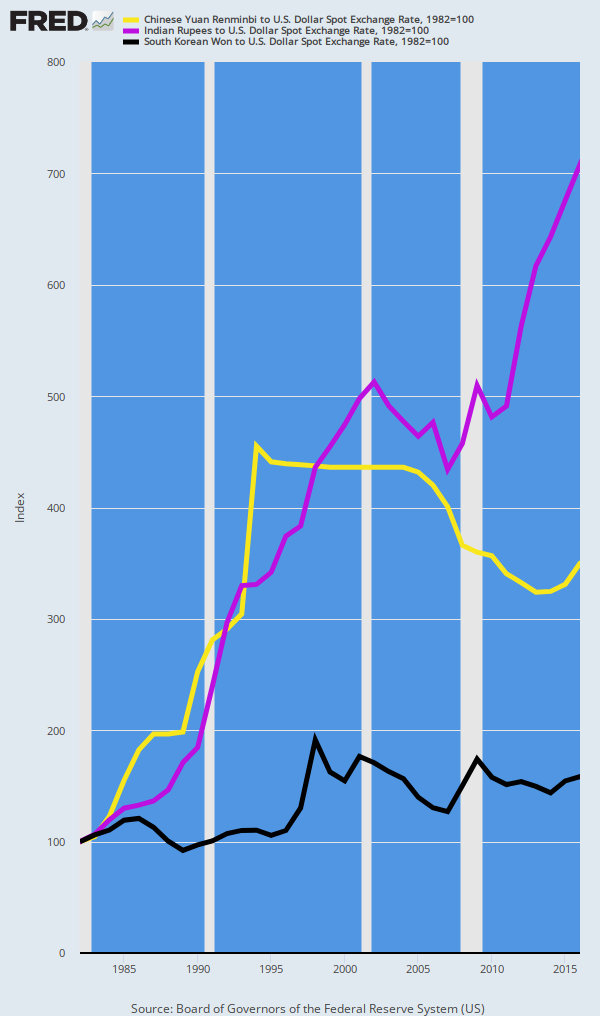

The result is illustrated by the chart below, which indexes the South Korean won, the Chinese yuan and the Indian rupee to a 1982 value of 100. During the next 34 years through 2016, the US CPI rose by a blistering 123%. So according to the textbooks the USD should have weakened and bought fewer and fewer won, yuan and rupee over time—meaning that the indexed lines in the chart should have been trending downward from the starting point of 100.

As is evident, just the opposite happened. By the eve of the Donald’s arrival at the White House the US dollar was buying 1.6X more won, 3.5X more yuan and 7.1X more rupees than it had in 1982. And, in turn, that meant even more off-shoring of US jobs and production to these low-wage economies.

After all, with a stronger won, yuan or rupee the dollar cost of goods or services originated in these countries would have been higher. In turn, that would have narrowed the gap with US based production costs, which reflected the 15o% rise in the CPI and 170% rise in average hourly US wages during that period. As it happened, however, the considerably weaker exchange rates in the export currencies shown in the graph below actually widened the competitive gap.

Transmission of the Fed’s Bad Money Disease, 1981 to 2016

In the case of what we have called the Mexican Assembly Price, the widening of the dollar cost gap owing to Mexico’s rampant money-printing and exchange rate depreciation had been even more dramatic. When Greenspan launched what amounted to Keynesian monetary policy after mid-1987, Mexican workers were earning pesos worth 74 cents, but by the time the Donald took office their peso earnings were worth only 5 cents.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.