Rogue Central Banking In Several Lessons, Part 2

Once the inflation genie was out of the bottle with the CPI clocking in at 6.0% by the fall of 1970, the Fed struggled for more than a decade to put it back. Consequently, any focus on stimulating growth, jobs, housing and investment was infrequent and definitely secondary to inflation-fighting.

We amplify the 1970s flood of central bank money and the resulting inflationary mess below, but it is important to note at the onset that despite four recessions (1970, 1975, 1980 and 1981) and very little pro-growth help from an inflation-preoccupied Fed, the US economy did expand at a decent clip during the interval between Q4 1969 and Q2 1987.

The per annum growth rate (real final sales basis) averaged a solid 3.1%, but that occurred due to the inherent growth propensities of private capitalism and despite the roadblocks thrown up by periodic bouts of monetary stringency. In fact, three Fed chairman served during that 17.5-year interval—Burns, Miller and Volcker—and with varying degrees of success their focus was overwhelmingly on suppressing inflation, not goosing growth.

As it happened, the growth rates of jobs, productivity and real median family income during this period were not especially outstanding, but these metrics didn’t plunge into an economic black hole, either. Self-evidently, these outcomes on main street were the work of market capitalism, not the central bank. The latter was leaning hard against inflation during most of the period—so this absence of central bank “help” is just further proof that easy money stimulus is not necessary for solid growth and main street prosperity.

Per Annum Change, Q4 1969 to Q2 1987

Real Final Sales of Domestic Product: +3.1%.

Labor hours employed: +1.5%.

Nonfarm productivity: +1.8%.

Real Median Family Income: +1.2%.

For avoidance of doubt, here is the path of the Federal funds rate as the above macroeconomic performance was unfolding. To wit, the Fed’s recurrent anti-inflation initiatives caused the funds rate to gyrate wildly like some kind of monetary jumping bean. In the run-up to each of the four recessions designated by the shaded areas of the graph, the increase in the Fed funds rate was as follows:

1970: +340 basis points.

1974: +960 basis points.

1980: +1,290 basis points.

1981: +440 basis points.

Needless to say, these successive rate-raising campaigns amounted to hammer blows to the main street economy. There is no way that these violent interest rate swings and the consequent start and stop economic cycles—four recessions in only 17 years— were a tonic for growth during this era of high and volatile inflation.

In effect, the reasonably solid macroeconomic performance quantified above represents a kind of free market minimum. It reflects the relentless drive of workers, consumers, entrepreneurs, businessmen, investors, savers and speculators to better their economic circumstances—even in the face of inflationary roadblocks and anti-inflation financial manipulation by the central bank.

Federal Funds Rate, August 1968 to June 1987

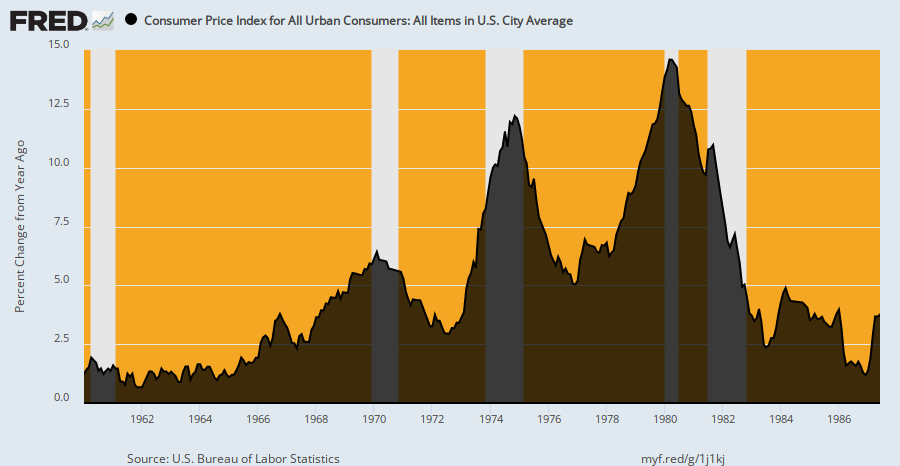

Of course, the inflationary roadblocks were enormous, and far beyond any prior peacetime experience. Compared to the 1.3% inflation average during 1951 to 1962, the CPI rose at a 5.6% rate over 1969:4 to 1987:2.

And that included the benefit of the sharp drop in inflation engineered by Paul Volcker during the final four years of the period. Thus, during the decade of the 1970s through the Y/Y inflation peak at 14.6% in April 1980, the CPI rose by an average of 7.7% per annum.

In turn, this introduced the wage-earning classes for the first time to the treadmill of robustly rising nominal wage rates, which become almost entirely consumed by sharply rising consumer prices. Thus, during the decade ending in the inflationary peak of Q2 1980, average hourly earnings in nominal terms rose by 7.6% per annum. But, alas, what stuck to the walls of workers’ bank accounts was a gain of only 1.1% per annum during the same period. All the rest was eaten up by inflation.

Y/Y Change In the CPI, 1960 to 1987

If the wage/price treadmill effect introduced after 1969 was the whole story, the impact might be considered minimally tolerable. The resilience of market capitalism was shown to be sufficiently strong so as to overcome much of the inflationary headwinds, along with the Fed’s punishing cycles of anti-inflation tightening.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.