Rogue Central Banking In Several Lessons, Part 1

What passes for central banking today is really a perverse form of Wall Street-pleasing monetary manipulation. We describe it as “rogue” because it employs the vocabulary of central banking, but in practice it fundamentally undermines main street prosperity, even as it showers the 1% with unspeakable financial windfalls.

So here’s the first and most important lesson as to why today’s form of rogue central banking is utterly unnecessary, and, in fact, is a huge roadblock to restoring fiscal sanity, financial sustainability and middle-class prosperity in America.

This lesson begins with startling historical proof that the post-war US economy did just fine without any interest rate targeting, heavy-duty bond-buying or general macroeconomic management help from the Fed at all. For all practical purposes today’s Fed domination of the financial and economic system was non-existent at the time.

We are referring to the full decade between Q4 1951 and Q3 1962 when the balance sheet of the Fed remained flat as a board at just $51 billion (black line). Yet the US economy did not gasp for lack of monetary oxygen. GDP grew from $356 billion to $609 billion or by 71% (purple line) during the period. That’s nominal growth of 5.1% per annum, and the majority of it represented real output gains, not inflation.

As it happened, this halcyon span encompassed the immediate period after the so-called Treasury-Fed Accord of March 1951, which finally ended the WWII expedient that had pegged Treasury bills at 0.375% and the long-bond at 2.5o% in order to finance the massive flow of war debt. Accordingly, in the post-peg period shown below interest rates were allowed by a newly liberated Fed to find their own market clearing levels.

Change in Federal Reserve Balance Sheet Versus GDP, Q4 1951 to Q3 1962.

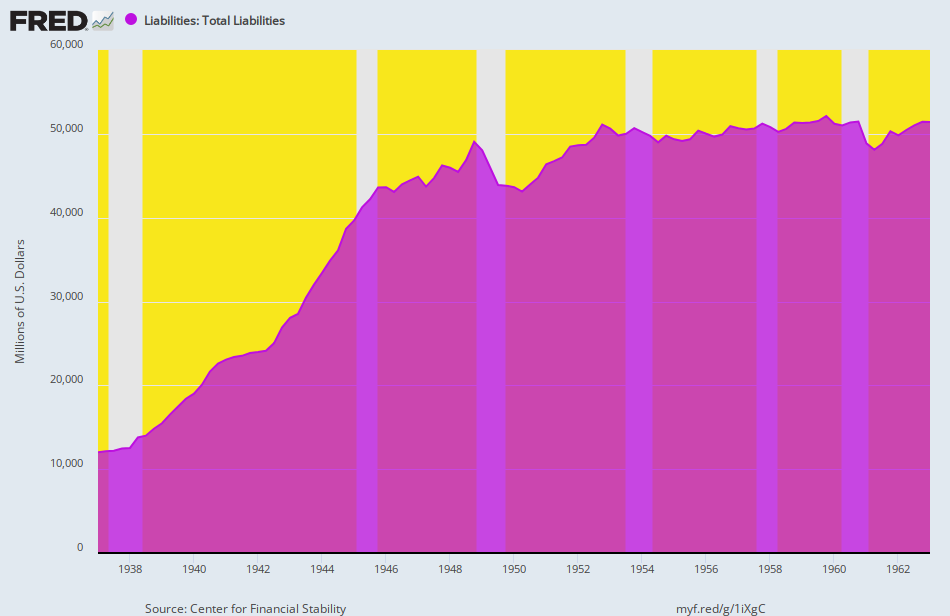

The effect of the WWII pegs, of course, was that the Fed had been obliged to absorb any and all US Treasury supply that did not clear the market at the target yields. Not surprisingly, the Fed’s 1937 balance sheet of $12 billion had risen by 4.3X to $51 billion by the time of the Accord, thereby reflecting what amounted to the original version of backdoor monetization of the public debt.

As it happened, the Treasury department official who negotiated the Accord and brought an end to the massive wartime debt monetization depicted below was William McChesney Martin. His father had been one of the authors of the 1913 Federal Reserve Act and had become president of the St. Louis Federal Reserve just before the trauma of the 1929 crash. Martin followed his father’s footsteps to Wall Street and became president of the New York Stock Exchange at the tender age of 31, where he spent the better part of the decade coping with the economic and financial wreckage that had ensued from the financial excesses of the Great War and the Roaring Twenties.

So upon becoming Chairman of the newly liberated Federal Reserve shortly after the 1951 Accord, Martin was already steeped in the lessons of the 1929 crash and was not about to accommodate a new outbreak of financial speculation. Hence, the Fed’s balance sheet remained on the straight and narrow during the first decade of his tenure.

But, alas, Martin’s vigilant insistence on keeping the Fed’s printing presses on idle did not prevent the US economy from generating a powerful tide of growth, investment, productivity and rising real wages and main street living standards. Moreover, owing to minimal money-printing, CPI inflation was exceedingly tame at just 1.3% per annum—a sustained main street respite from inflation never to be recorded again.

Indeed, the combination of high growth, robust investment, strong wages and smartly rising real family income, on the one hand, and rock-bottom inflation on the other, surely constitutes the gold standard of performance for a modern capitalist economy.

And yet, and yet. It was all accomplished under a regime of persistent “light touch” central banking that assumed free market capitalism would find its own way to optimum economic growth, employment, housing, investment and main street prosperity. No monetary Sherpa at the Eccles Building was necessary.

Per Annum Change, Q4 1951 to Q3 1962

Real Final Sales: +3.8%.

Real Domestic Investment: +4.1%.

Nonfarm productivity growth: +2.5%.

Real hourly wages: +3.0%.

Real Median Family Income: +2.3%.

CPI Increase: +1.3%

Federal Reserve Liabilities, 1937 to 1962

There is absolutely nothing about this period that makes the superior macroeconomic peformance summarized above aberrational, flukish or unreplicable.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.