Bubbles R-Us

The Wall Street Journal today brings word that a professor Efraim Benmelech of the finance department at Northwestern University thinks the Fed is hurting housing and the consumer too much. Opined he,

…….those higher interest rates are making mortgages more expensive and leading to fewer home sales. That leads to less spending on appliances, paint and other home goods, because people commonly buy those items ahead of a sale and after moving.

“The actions of the Fed are leading to lower consumption,” he said.

You don’t say!

Then again, has it occurred to the good professor that the years and years of ultra low mortgage rates engineered by the Fed were totally unnatural, uneconomic and not sustainable?

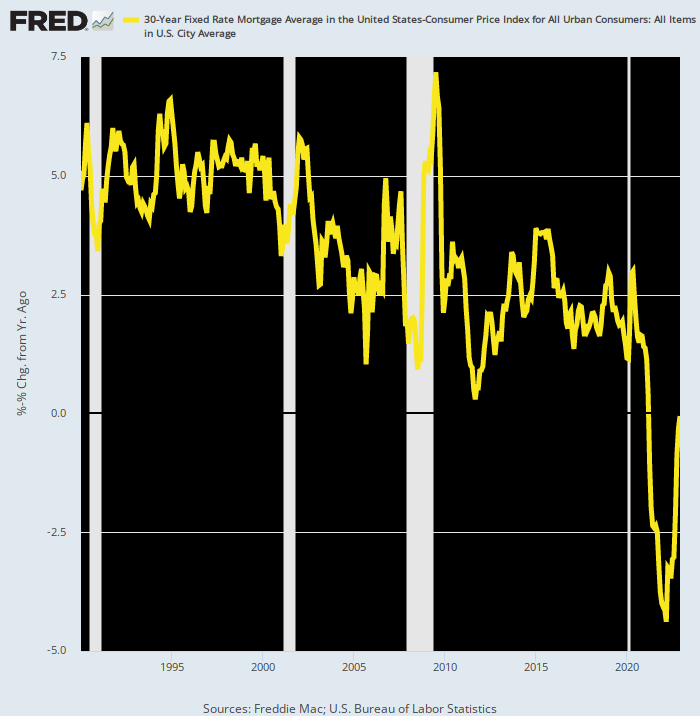

The evidence for that is in the chart below. It shows that for most of the last three decades, the Fed drove the after-inflation or “real” interest rate on 30-year mortgages steadily lower until it actually turned negative.

That’s right. There was a whole lot of appliances, paint and other building supplies being sold because mortgage investors were getting fleeced by the Fed’s negative real rate regime. But now it’s time to pay the piper.

Stated differently, the unfolding recession is a long overdue and necessary purge of artificial economic activity stimulated and subsidized by the central bank’s own financial repression policies.

The Fed’s belated attempt to “normalize” interest rates, therefore, is not a mean-spirited policy to deliberately cause labor, manufacturing capacity and other economic resources to be idled. To the contrary, it’s a belated attempt to unshackle markets from the excesses, bubbles, malinvestments, inefficiencies and unsustainabilities that were the inherent results of decades of reckless money-printing.

Inflation-Adjusted Interest Rate On 30-Year Fixed Rate Mortgages, 1990 to2023

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.