Another Punk Jobs Report—But Not A Dime’s Worth Of UniParty Difference

The monthly jobs report is always loaded with information demonstrating that Washington’s endless fiscal and monetary stimmies have done absolutely nothing to improve the nation’s once and former prosperous private enterprise economy. And the report for October released on Friday did not disappoint.

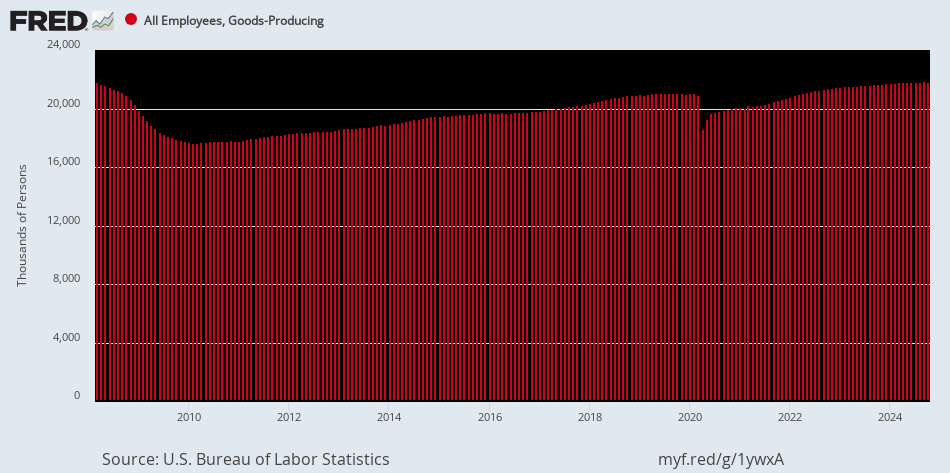

For instance, way back in March 2008 there were 21.819 million goods-producing jobs in the US, which figure posted at 21.821 million for October 2024. That’s a mere 2,000 job gain in the last 199 months in the manufacturing, construction, energy and mining industries combined. The resulting math of it is quite astounding: The growth rate has averaged 10 goods-producing jobs per month.

And that’s T-E-N, as in the number of fingers on two hands. No zeroes deleted!

Moreover, this is not a mere statistical curiosity. A typical job in the good-producing sector pays an average gross wage of nearly $67,000 per year. By contrast, the employment level in the low pay/low productivity Leisure and Hospitality (L&H) sector during the same 16-year period has risen from 13.5 million to 17.0 million or by 26%. The again, the average annual pay rate in the L&H sector is only $29,500 or just 44% of the pay rate in the flat-lining goods-producing sectors.

So, no, the Fed is not simulating prosperity with its endless money-printing and financial repression escapades. What we have had over that period, instead, is a lot of inflation, huge off-shoring of middle class jobs, explosive growth of the public debt, endless financial engineering in the corporate sector and unspeakable windfall wealth showered upon the top 1%.

Employment In Goods-Producing Sectors, 2008 to 2024

For want of doubt, here is the change in net worth as between the top 1% of households and the bottom 50% during the same 199 month period after March 2008. As shown in the purple area of the graph, net worth at the tippy-top of the economic ladder has soared from $18.3 trillion to $46.7 trillion. That’s a gain of $28.4 trillion for the top 1.33 million households or $21.4 million each.

When it comes to the bottom 50% (black area), not so much. The 66.5 million households in the bottom half of the distribution have gained just $2.9 trillion of net worth, or about $44,000 per household. In round terms, that’s a 500:1 ratio on a per household basis.

Here’s the thing. On its own steam, there is no way that an economy that has generated zero high pay/high productivity jobs over the last 16.6 years could have also legitimately generated a $28.4 trillion net worth gain for the tiny number of households at the top of the economic ladder. The chart below is evidence of massive asset inflation, pure and simple.

Keep reading with a 7-day free trial

Subscribe to David Stockmans Contra Corner to keep reading this post and get 7 days of free access to the full post archives.